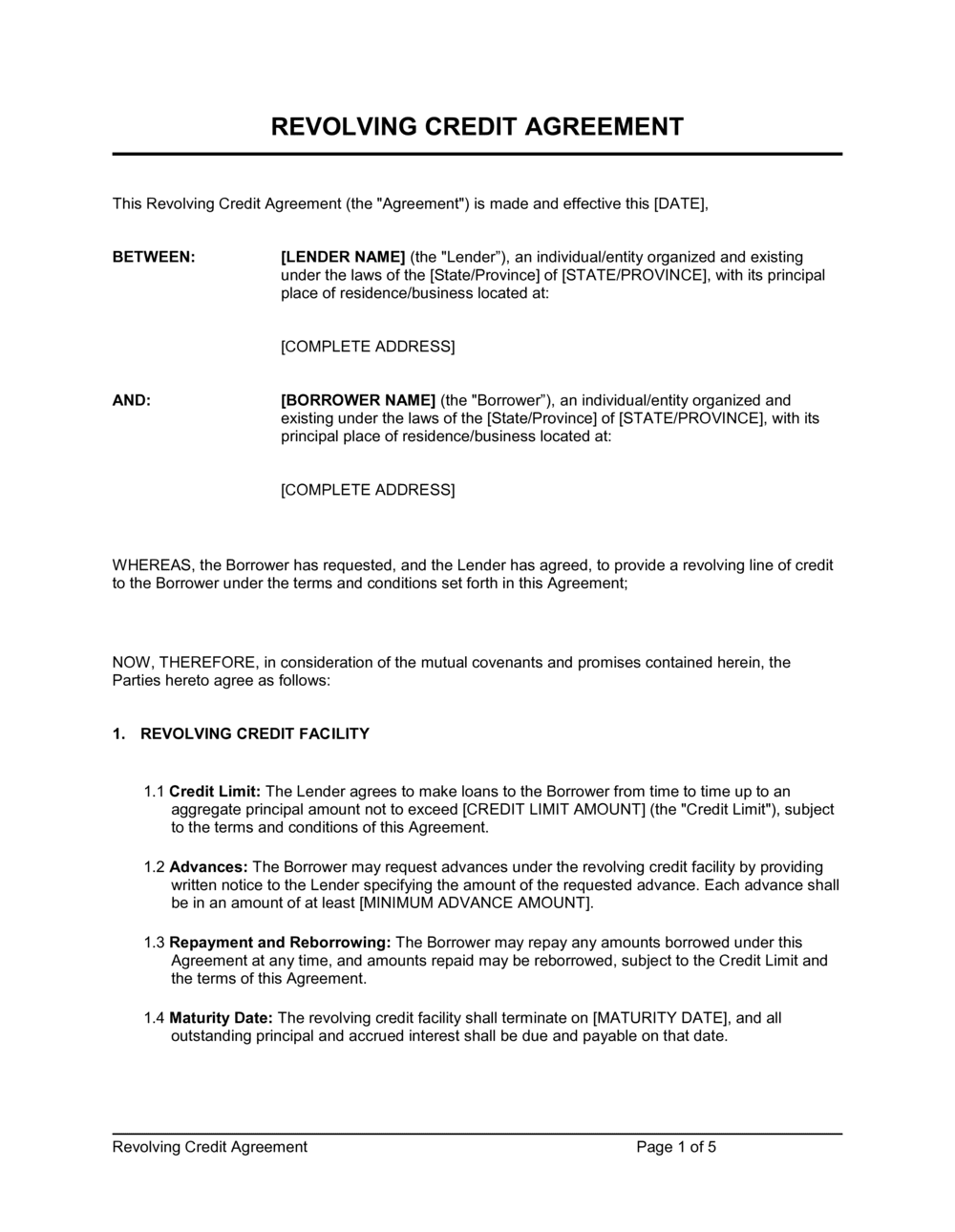

In the dynamic landscape of modern commerce, businesses often require flexible access to capital to manage cash flow, seize opportunities, and navigate unexpected challenges. A revolving credit facility stands as a cornerstone of such financial agility, offering a line of credit that can be drawn upon, repaid, and redrawn, much like a business credit card but typically on a larger scale and with more structured terms. This financial instrument is invaluable for working capital needs, inventory financing, or simply as a robust liquidity backstop.

However, the efficacy and safety of such a facility hinge entirely on the underlying legal documentation. Without a meticulously crafted agreement, both lenders and borrowers face significant risks, from misunderstandings about repayment schedules to disputes over interest rates or collateral. A robust revolving credit facility agreement template serves as the foundational blueprint, providing clarity, outlining mutual obligations, and establishing a legally enforceable framework that protects all parties involved. It’s an essential tool for financial institutions, corporate treasurers, in-house legal departments, and external legal counsel seeking efficiency and precision in their deal-making.

The Imperative of Formal Documentation in Today’s Business

In an era defined by rapid transactions and intricate financial instruments, the reliance on handshake deals or informal understandings is not just risky, it’s often catastrophic. A clear, written agreement provides an unambiguous record of the terms and conditions, eliminating ambiguities that can lead to costly litigation or irreparable damage to business relationships. For a complex financial arrangement like a revolving credit facility, this formal documentation is not merely a formality but a critical safeguard.

A comprehensive contract ensures that all parties, from the borrower to the lender, have a unified understanding of their rights, responsibilities, and the mechanisms for dispute resolution. It acts as a reference point for compliance, performance monitoring, and risk management. In the highly regulated US financial environment, robust documentation is also crucial for satisfying regulatory requirements and demonstrating due diligence.

Core Advantages of a Standardized Agreement Framework

The strategic adoption of a high-quality revolving credit facility agreement template offers a multitude of benefits that extend beyond mere legal compliance. Primarily, it introduces a level of standardization and efficiency into the deal-making process. Rather than drafting each agreement from scratch, which is time-consuming and prone to errors, a well-structured template allows legal and finance teams to expedite negotiations and execution.

Moreover, such a template provides significant legal protections for both the borrower and the lender. It clearly delineates the terms of the credit, including interest rates, fees, repayment schedules, and events of default, thereby minimizing the potential for future disputes. For lenders, it secures their investment by outlining collateral requirements and borrower covenants, while for borrowers, it clarifies their obligations and rights, ensuring transparent and predictable access to funds. This proactive approach to documentation significantly reduces transactional risk and fosters greater confidence among all stakeholders.

Adapting the Framework to Diverse Business Needs

While a standardized revolving credit facility agreement template provides a strong foundation, its true value often lies in its adaptability. Businesses operate across a vast spectrum of industries, each with unique operational models, asset classes, and risk profiles. A flexible template allows for the seamless integration of industry-specific clauses and conditions, ensuring the agreement accurately reflects the particular nuances of, say, a manufacturing operation versus a software-as-a-service provider.

Customization extends to various financial scenarios as well. A facility for a rapidly growing tech startup might include different performance covenants than one for a mature, asset-heavy industrial firm. Similarly, adjustments can be made for secured versus unsecured facilities, specific borrowing base calculations, or tailored repayment triggers. The ability to modify sections pertaining to collateral, reporting requirements, or even the governing law ensures the document remains relevant and enforceable, regardless of the unique commercial context.

Key Provisions for Any Facility Document

A robust revolving credit facility agreement is a comprehensive document that articulates every aspect of the lending relationship. While specific terms will vary, certain essential clauses form the backbone of any sound agreement. These provisions ensure clarity, protect all parties, and establish a clear framework for the entire credit lifecycle.

Every well-drafted agreement should include:

- Parties and Definitions: Clearly identify the borrower(s), lender(s), and any guarantors, along with precise definitions for key terms used throughout the agreement (e.g., “Business Day,” “Event of Default,” “Borrowing Base”).

- Facility Amount and Commitment: Specify the maximum aggregate principal amount that can be drawn under the facility and the period for which the lender is committed to making funds available.

- Interest Rates and Fees: Detail the applicable interest rates (e.g., SOFR-based, Prime), calculation methods, any default interest rates, and all associated fees (e.g., commitment fees, unused facility fees, agency fees).

- Drawdowns and Repayment: Outline the mechanics for requesting advances, conditions precedent to each drawdown, and the schedule and methods for principal and interest repayment.

- Representations and Warranties: Statements of fact made by the borrower at the time of signing and often reaffirmed at each drawdown, concerning its legal status, financial condition, absence of litigation, and compliance with laws.

- Affirmative Covenants: Obligations of the borrower to perform certain actions, such as maintaining insurance, providing financial statements, paying taxes, and complying with laws.

- Negative Covenants: Restrictions on the borrower’s actions, such as limitations on incurring additional debt, granting liens, making acquisitions, or paying dividends without lender consent.

- Events of Default: Clearly define circumstances that trigger a default, allowing the lender to accelerate repayment or exercise other remedies (e.g., failure to pay, breach of covenant, insolvency, cross-default).

- Collateral and Security: If the facility is secured, detail the assets pledged as collateral, the security interests granted, and the procedures for enforcement in case of default.

- Indemnification: Provisions where the borrower agrees to protect the lender from certain liabilities, losses, or expenses related to the credit facility.

- Governing Law and Jurisdiction: Specify the state laws that will govern the interpretation and enforcement of the agreement, and the courts that will have jurisdiction over disputes.

- Confidentiality: Clauses protecting sensitive information exchanged between the parties.

- Assignment: Rules regarding whether and how the lender can assign its rights or obligations under the agreement to another party.

- Amendments and Waivers: Procedures for modifying the agreement or waiving any of its provisions.

Enhancing Usability and Readability

Beyond the legal substance, the practical presentation of a revolving credit facility agreement template significantly impacts its effectiveness. A document that is difficult to navigate or understand can lead to misunderstandings, delays, and errors, even if its underlying legal framework is sound. Therefore, careful attention to formatting, usability, and readability is paramount for both print and digital applications.

Employing clear, logical headings and subheadings (like the structure of this article itself) helps stakeholders quickly locate relevant sections. Consistent typography, adequate white space, and judicious use of bullet points or numbered lists break up dense text, making the content less intimidating and easier to digest. For digital use, ensuring the document is searchable (e.g., a properly OCR’d PDF), includes internal hyperlinks for cross-references, and is compatible with common document management systems enhances its utility. A well-formatted agreement reflects professionalism and facilitates smoother review and execution by all parties, from legal counsel to finance teams.

The complexities of financial transactions in today’s business environment demand precision, clarity, and legal rigor. Utilizing a well-structured revolving credit facility agreement template is not merely a convenience; it is a strategic imperative for any entity engaged in significant lending or borrowing activities. It provides a robust framework that minimizes risk, ensures compliance, and fosters transparent, predictable financial relationships.

By investing in or developing a high-quality template, businesses and financial institutions can streamline their operations, reduce legal costs, and significantly enhance their confidence in financial dealings. This proactive approach to documentation empowers all parties to focus on growth and strategic objectives, secure in the knowledge that their financial arrangements are built on a solid, legally sound foundation. A professionally crafted template is therefore more than just a document; it’s an essential tool for effective and secure financial management.