Navigating the financial landscape of a small business can often feel like steering a ship through a dense fog. Without a clear map, it’s easy to drift off course, make impulsive decisions, or worse, run aground. Many entrepreneurs start with passion and a great idea, only to find the complexities of managing money overwhelming. This is where a structured approach becomes indispensable, transforming uncertainty into clarity and helping business owners plot a reliable path forward.

A robust financial framework isn’t just about tracking expenses; it’s about strategic foresight, empowered decision-making, and securing the long-term viability of your venture. For busy entrepreneurs, an effective Budget Template For Small Business isn’t just a nicety—it’s a critical tool. It provides a foundational structure, allowing you to allocate resources wisely, identify potential shortfalls before they become crises, and understand the true financial health of your operations. This article will guide you through the essentials of building and utilizing such a template, ensuring your business sails smoothly toward its goals.

Why Every Small Business Needs a Financial Roadmap

In the dynamic world of small business, uncertainty can be a constant companion. From fluctuating market demands to unexpected operational costs, without a clear financial roadmap, businesses operate largely on guesswork. A well-crafted financial plan provides the necessary structure to anticipate income, manage expenditures, and make informed choices about growth and investment. It acts as an early warning system, highlighting potential cash flow issues long before they escalate into serious problems.

Beyond mere solvency, a comprehensive financial management tool empowers business owners to set realistic goals and measure progress against them. It helps in evaluating the profitability of different products or services, pinpointing areas where costs can be reduced, and identifying opportunities for strategic investment. This proactive approach to financial health is not just about survival; it’s about fostering sustainable growth and building a resilient business that can withstand economic fluctuations and capitalize on new opportunities.

The Power of a Structured Financial Plan

Implementing a structured financial plan offers a multitude of benefits that extend far beyond simply keeping track of money. Firstly, it provides unparalleled **clarity** regarding your financial inflows and outflows. You gain a precise understanding of where every dollar comes from and where it goes, eliminating guesswork and providing a solid basis for decision-making. This transparency is crucial for both day-to-day operations and long-term strategic planning.

Secondly, a well-defined financial framework significantly improves resource allocation. By seeing the full financial picture, you can direct funds to the most impactful areas of your business, whether it’s marketing, product development, or operational improvements. This strategic distribution of capital ensures that your investments yield the highest possible return. Furthermore, it allows for proactive identification of potential financial inefficiencies or areas where spending might be excessive, enabling timely adjustments and cost-saving measures. Finally, having a solid business budget spreadsheet can instill confidence, not only for the business owner but also for potential investors or lenders who require evidence of sound financial management before committing capital.

Key Components of an Effective Small Business Budget

To be truly effective, any small business financial roadmap must encompass several critical elements. These components work together to provide a holistic view of your financial standing, enabling accurate forecasting and strategic planning. Customizing these elements to your specific industry and business model is key to its utility.

Here are the essential components to include in your financial management template:

- **Revenue Streams:** Detail all sources of income, whether from product sales, service fees, subscriptions, or other operational activities. Break down revenue by category to understand your most profitable avenues.

- **Fixed Expenses:** These are costs that generally remain constant each month, regardless of your sales volume. Examples include **rent**, salaries (for permanent staff), insurance premiums, loan payments, and software subscriptions.

- **Variable Expenses:** Unlike fixed expenses, these costs fluctuate with your business activity. This category includes **raw materials**, shipping costs, marketing spend (if campaign-dependent), hourly wages for contract workers, and utility bills that vary with usage.

- **One-Time and Capital Expenditures:** Account for significant, infrequent purchases such as **new equipment**, major software licenses, vehicle acquisitions, or office renovations. These are crucial for long-term planning and asset management.

- **Cash Flow Projections:** This section forecasts the movement of cash into and out of your business over a specific period. It helps you anticipate periods of surplus and deficit, allowing for **proactive management** of working capital.

- **Profit & Loss (P&L) Analysis:** A vital component for comparing your budgeted figures against actual performance. This analysis helps identify discrepancies, assess profitability, and make necessary adjustments to your financial planning.

- **Contingency Fund:** Allocate a portion of your budget for unexpected events, such as equipment breakdowns, economic downturns, or sudden market shifts. A **robust contingency fund** acts as a financial safety net.

- **Debt Repayment Schedule:** If your business carries debt, include a clear plan for repayment. This ensures you meet obligations and work towards a healthier **debt-to-equity ratio**.

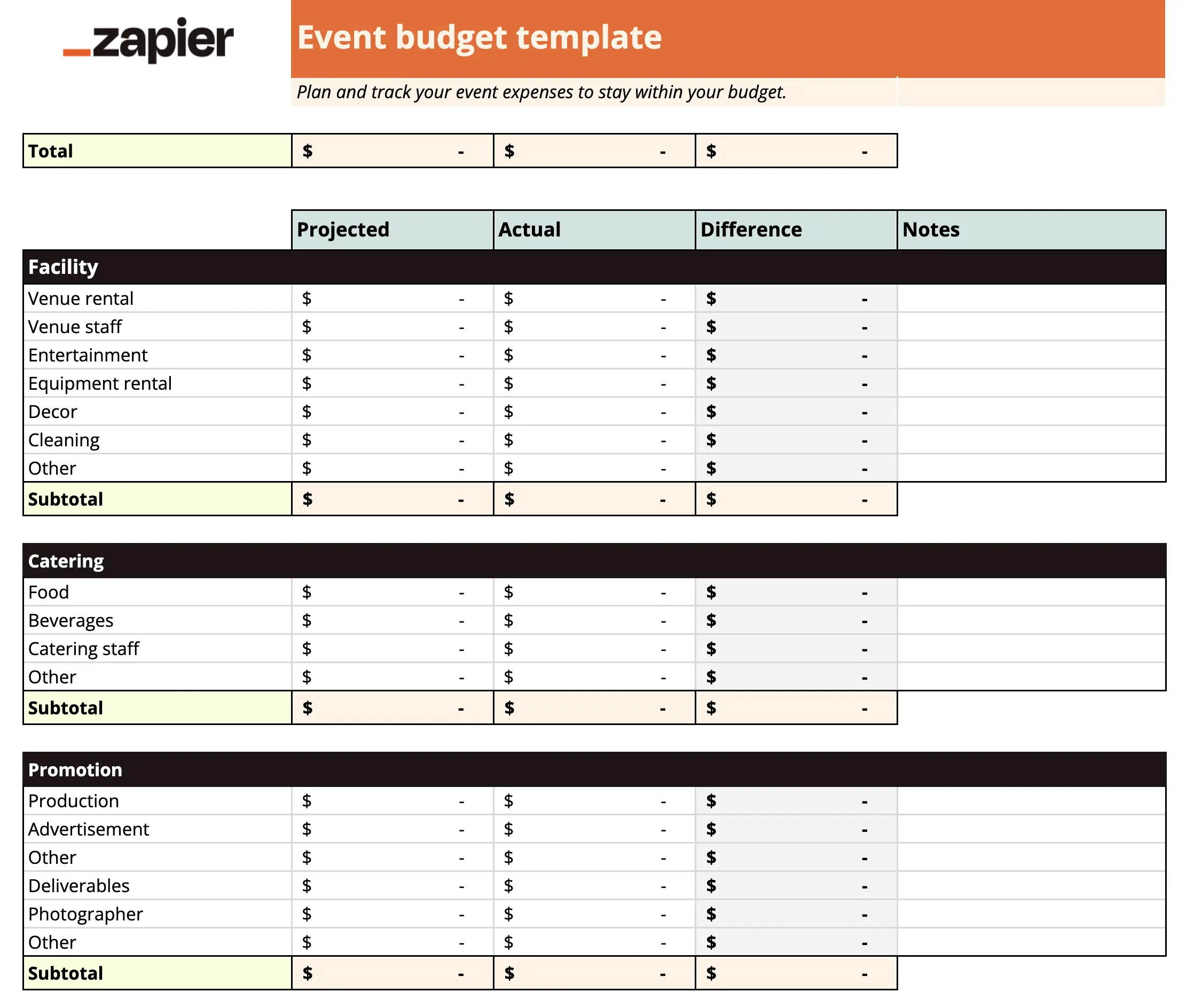

Choosing and Customizing Your Financial Planning Tool

Selecting the right financial planning tool for your small business is a crucial step in establishing robust fiscal control. While many general templates are available, the ideal solution is one that can be tailored to the unique intricacies of your business model. You might opt for a sophisticated accounting software package that integrates budgeting features, or perhaps a more straightforward spreadsheet-based system if your needs are simpler. Many entrepreneurs find that an adaptable Excel or Google Sheets template provides the perfect balance of flexibility and structure.

When evaluating options, consider the ease of use and your team’s familiarity with the software. Look for features that allow for easy input of data, automated calculations, and visual representations of your financial health. Crucially, the ability to customize categories for income and expenses is paramount. Your small business budget should reflect your operational realities, not a generic model. This might mean adding specific line items for industry-specific licenses, unique marketing channels, or niche inventory costs. A well-chosen and thoroughly customized budgeting process for entrepreneurs ensures that the tool serves your business effectively, providing actionable insights rather than just raw data.

Tips for Successful Budget Implementation and Maintenance

Creating a budget is only the first step; successful implementation and ongoing maintenance are what truly drive financial success. A small business budgeting tool is not a static document; it’s a living blueprint that requires regular attention and adjustment to remain relevant and effective.

Here are some key tips to ensure your financial health tool works for you:

- Start Simple and Grow: Don’t get overwhelmed trying to account for every single penny from day one. Begin with the major income streams and expenses, then gradually add more detail as you become comfortable. A basic financial blueprint is better than no plan at all.

- Be Realistic, Not Optimistic: When forecasting revenue, err on the side of caution. For expenses, try to overestimate slightly. This conservative approach helps avoid unpleasant surprises and ensures you’re prepared for potential downturns.

- Track Everything Regularly: The effectiveness of your expenditure tracking sheet hinges on consistent data input. Make it a routine to log all income and expenses daily or weekly. This habit provides accurate insights and makes monthly reconciliation much smoother.

- Review and Adjust Monthly/Quarterly: Your business environment is constantly changing. Schedule regular reviews (monthly or at least quarterly) to compare actual performance against your budget. Identify variances, understand their causes, and adjust your future forecasts accordingly.

- Use it as a Decision-Making Tool: Don’t just file your fiscal planning sheet away. Actively use it to guide decisions on hiring, purchasing new assets, investing in marketing campaigns, or even evaluating the profitability of new product lines.

- Involve Key Team Members: If you have employees, especially in finance or management roles, involve them in the budgeting process. Their insights can be invaluable, and their buy-in will ensure better adherence to the financial model for small businesses.

- Separate Business and Personal Finances: This might seem obvious, but it’s a common pitfall for new entrepreneurs. Maintain distinct bank accounts, credit cards, and financial records for your business to simplify tracking and ensure accuracy.

Common Pitfalls to Avoid When Managing Your Finances

Even with the best intentions and a robust budget template, small business owners can encounter common stumbling blocks that derail their financial management efforts. Being aware of these pitfalls can help you steer clear and maintain a healthy fiscal position. One of the most significant errors is **not having a budget at all**, leaving businesses vulnerable to unexpected costs and missed opportunities.

Another frequent misstep is creating an unrealistic budget. Overly optimistic revenue projections or underestimation of costs can lead to constant shortfalls and frustration. It’s crucial to base your operational budget guide on historical data and current market realities, rather than wishful thinking. Many businesses also fail by creating a budget and then ignoring it. A budget is a living document; it loses its value if not regularly monitored, updated, and used as a guide for decision-making. Neglecting to track actual income and expenses against the budget means missing vital opportunities to identify issues and make timely adjustments. Finally, mixing personal and business finances, failing to build a contingency fund, or not accounting for taxes and other statutory deductions are common oversights that can lead to significant financial stress down the line.

How often should I update my small business budget spreadsheet?

While the initial creation of your budget is a substantial task, its true value comes from ongoing maintenance. You should aim to review and update your financial plan monthly. This allows you to compare actual performance against your projections, identify any significant variances, and make necessary adjustments to future forecasts. A quarterly deep dive for more strategic reviews is also highly recommended.

Can a startup benefit from a financial planning template?

Absolutely. Startups, perhaps more than any other business, need a solid financial planning template. They often operate with limited funds and face significant initial expenses. A detailed startup budget plan helps entrepreneurs understand their burn rate, forecast when they’ll need additional funding, and prioritize spending to ensure their capital lasts as long as possible while they build and scale their business.

What if my actuals always differ significantly from my budget?

Consistent and significant variances between your budgeted figures and actual performance indicate that your forecasting methods may need adjustment. It’s important not to see this as a failure, but rather as an opportunity for learning. Analyze *why* the variances occurred: were your revenue projections too high, or did expenses unexpectedly surge? Use these insights to refine your future budgets, making them more accurate and realistic. It might also signal a need to re-evaluate your business model or operational costs.

Should I include my salary in my operational budget guide?

Yes, if you, as the business owner, are taking a salary or drawing a regular wage from the company, it should absolutely be included as an expense in your operational budget guide. Treating your compensation as a business expense ensures that your budget accurately reflects the true cost of operating your business and helps maintain clear financial boundaries between your personal and business finances.

Embracing a robust financial planning framework, such as a well-designed Budget Template For Small Business, is not just a best practice—it’s a fundamental pillar of entrepreneurial success. It equips you with the foresight to navigate challenges, the clarity to seize opportunities, and the control to build a sustainable, profitable enterprise. This systematic approach transforms financial management from a daunting chore into an empowering strategic advantage.

Don’t let the complexities of money management hold your business back. Take the proactive step today to implement a comprehensive financial framework. By doing so, you’re not just creating a document; you’re forging a clear path to financial stability, informed growth, and the lasting success of your small business.