Self-employment offers unparalleled freedom and the thrill of building something of your own, but it also comes with a unique set of financial challenges. Unlike traditional employees, independent contractors, freelancers, and small business owners navigate fluctuating income, self-funded benefits, and significant tax responsibilities without the safety net of a regular paycheck or an HR department. Managing personal and business finances can quickly become overwhelming, making a clear, actionable plan not just helpful, but absolutely essential for long-term success and peace of mind.

This is where a dedicated financial framework, such as a Monthly Budget Template For Self Employed Td, steps in as your indispensable co-pilot. It’s more than just a spreadsheet; it’s a strategic tool designed to bring clarity to your cash flow, demystify your tax obligations, and empower you to make informed decisions about your future. By meticulously tracking every dollar in and out, you gain the control necessary to stabilize your financial footing, plan for growth, and ensure your entrepreneurial journey remains both rewarding and sustainable.

The Unique Financial Landscape of Self-Employment

The path of a self-employed individual is distinct from that of a traditional employee, especially concerning finances. Income streams can be highly variable, often flowing in unpredictably based on client projects, sales cycles, or seasonal demand. This inherent variability makes consistent financial planning a complex, yet critical, endeavor. Without a steady paycheck, estimating future earnings requires a robust system.

Furthermore, self-employed individuals are solely responsible for a host of expenses and obligations typically covered or subsidized by an employer. This includes the full brunt of health insurance premiums, retirement contributions, and the employer portion of Social Security and Medicare taxes. Understanding these unique costs is the first step toward building a sustainable financial model.

Tax obligations also present a significant difference. As a self-employed individual, you are responsible for paying estimated taxes quarterly to cover income and self-employment taxes. Miscalculating or failing to set aside enough funds for these payments can lead to substantial penalties and unexpected financial strain. A precise budgeting tool helps you allocate funds consistently, ensuring you’re always prepared.

Finally, the blurring lines between personal and business finances is a common pitfall. Without clear separation and tracking, it becomes difficult to assess business profitability, identify legitimate deductions, or understand your true personal disposable income. A structured approach to managing both realms is paramount for clarity and compliance.

Why a Dedicated Budget Template is Your Best Ally

For the self-employed, a robust financial tracking system serves as the bedrock of financial stability and growth. It transforms abstract numbers into actionable insights, providing a clear snapshot of your financial health at any given moment. This level of transparency is invaluable for navigating the unpredictable nature of entrepreneurial income.

A well-crafted budgeting tool gives you unprecedented control over your cash flow. You can proactively identify where your money is going, optimize spending, and allocate resources more efficiently towards personal savings, debt reduction, or business investments. This proactive stance significantly reduces financial anxiety and fosters a sense of empowerment.

Moreover, having a detailed record of income and expenses simplifies tax preparation immensely. All the necessary data points are organized and readily accessible, making it easier to claim eligible deductions and accurately calculate your tax liability. This not only saves time but also minimizes the risk of errors and potential audits.

Ultimately, a dedicated budget acts as your financial compass, guiding your decisions and ensuring you stay on course toward your long-term goals. Whether it’s saving for a down payment, funding a child’s education, or expanding your business, a clear financial roadmap makes these aspirations attainable. It moves you from reactive money management to strategic financial planning, securing your future.

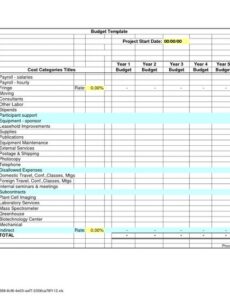

Key Components of an Effective Self-Employed Budget

Creating a budget that truly serves the unique needs of a self-employed individual requires more than just listing income and expenses. It demands categories that reflect both personal and business finances, alongside allocations for future obligations like taxes and savings. A comprehensive financial plan needs to be both detailed and flexible.

This integrated approach ensures that no critical aspect of your financial life is overlooked, providing a holistic view of your money. By breaking down your financial landscape into distinct, manageable categories, you gain the granularity needed to make informed decisions and maintain fiscal discipline. It transforms complex financial data into a clear and actionable blueprint.

Here are the essential categories that should be included in any effective financial management template for independent workers:

- **Projected Monthly Income**: A realistic estimate of earnings based on current contracts, historical data, and pipeline.

- **Actual Monthly Income**: The exact amount of money earned and received during the month, for comparison against projections.

- **Fixed Personal Expenses**: Regular, non-negotiable personal costs like rent/mortgage payments, utility bills, and insurance premiums.

- **Variable Personal Expenses**: Flexible personal spending categories such as groceries, dining out, entertainment, and personal care.

- **Fixed Business Expenses**: Recurring business costs like software subscriptions, web hosting fees, and business insurance.

- **Variable Business Expenses**: Business-related spending that fluctuates, including marketing campaigns, project-specific materials, and professional development.

- **Tax Savings Allocation**: A dedicated percentage of gross income set aside specifically for federal, state, and self-employment taxes.

- **Emergency Fund Contribution**: Regular transfers to build a financial cushion for unexpected personal or business setbacks.

- **Retirement Savings**: Consistent contributions to your self-funded retirement accounts, such as a SEP IRA or Solo 401(k).

- **Debt Repayment Goals**: Specific amounts allocated to actively reduce credit card balances, personal loans, or business debts.

Building Your Personalized Financial Roadmap

Embarking on the journey of disciplined financial management begins with gathering accurate data and setting realistic expectations. Don’t feel overwhelmed by the process; break it down into manageable steps that build upon each other. Your personalized financial roadmap will become clearer with each piece of information you integrate.

Begin by compiling all relevant financial documentation from the past three to six months. This includes bank statements, credit card statements, invoices, and expense receipts. Having this historical data will provide a clear picture of your income patterns and spending habits, forming the foundation of your budget. This comprehensive review is crucial for understanding your financial baseline.

Next, delineate all your income streams. Whether you have one primary client, multiple freelance gigs, or product sales, list every source of revenue. This exercise helps you understand the true scope of your earning potential and identify any seasonal or cyclical patterns that might affect your monthly cash flow. Understanding your revenue diversity is a powerful insight.

The next critical step is to categorize your expenses. Clearly distinguish between personal and business expenditures, and then further classify them as fixed or variable. This separation is vital for both personal financial clarity and for accurate business accounting and tax purposes. A well-organized expense structure is the backbone of an effective Monthly Budget Template For Self Employed Td.

With your data organized, set clear and achievable financial goals. These might include building an emergency fund, paying down debt, saving for a major purchase, or investing in your business. Your budget should be designed to help you actively work towards these goals, making them tangible rather than just aspirations. Assigning a specific amount to each goal helps you prioritize.

Finally, allocate specific amounts to each category in your budget. This is where you decide how much to spend, save, and invest based on your income and goals. Remember, this is a living document, so be prepared to make adjustments as your income or expenses change. The initial allocation is a starting point, not a rigid, unchangeable decree.

Leveraging Technology and Banking Tools for Seamless Tracking

In today’s digital age, managing your finances doesn’t have to be a tedious, manual process. Leveraging technology can significantly streamline your budgeting efforts, making it more efficient and accurate. Integrating your financial tracking with your banking services is a powerful way to ensure you have real-time data at your fingertips.

Many self-employed individuals benefit from using dedicated budgeting software or apps that link directly to their bank accounts and credit cards. These tools automatically categorize transactions, generate reports, and provide a clear overview of your financial situation without the need for manual data entry. This automation saves considerable time and reduces the likelihood of human error.

When considering a financial management system, think about its compatibility with robust banking platforms. A reliable financial management tool works best when it can seamlessly pull data from your primary financial institution, allowing for easy reconciliation and comprehensive financial snapshots. This smooth integration ensures that your budget reflects your most current financial activity.

For instance, seeking out a system that is effective as a Monthly Budget Template For Self Employed Td means looking for features that support separate business and personal accounts, easy transaction tagging, and perhaps even tax projection capabilities. The goal is to minimize administrative burden and maximize insights, turning financial tracking into an asset rather than a chore.

Digital record-keeping is another key advantage. By maintaining digital copies of invoices, receipts, and bank statements, you create an organized and easily searchable archive. This not only aids in budgeting but is also invaluable for tax preparation and any potential audits, ensuring you have a complete paper trail (or rather, a digital trail). Embracing these technological solutions empowers you to maintain fiscal control with greater ease.

Strategies for Variable Income Management

One of the biggest hurdles for the self-employed is the inconsistency of income. Unlike salaried employees, your monthly earnings can fluctuate wildly, making traditional fixed budgeting difficult. Specialized strategies are necessary to manage this variability effectively and maintain financial stability.

The "buffer account" strategy is highly effective for smoothing out income peaks and troughs. The idea is to build up a reserve fund that holds several months’ worth of essential living and business expenses. During high-income months, you deposit extra funds into this buffer. During leaner months, you draw from it to cover your fixed costs, ensuring consistent cash flow regardless of your current earnings.

Another approach is to budget based on your average income over the past six to twelve months. This method provides a more stable figure to work with, even if individual months vary. While it might mean saving more in high-income months to cover a potential deficit in low-income months, it offers a consistent baseline for planning your expenses. This long-term average approach reduces immediate stress.

Some self-employed individuals find success by creating income "tiers." This involves developing different budget scenarios for high, medium, and low-income months. Each tier outlines adjusted spending limits for variable expenses. This allows for flexibility and ensures that you can adapt your financial behavior quickly in response to your actual earnings, preventing overspending during lean times.

Regardless of the strategy chosen, the golden rule remains: prioritize essential expenses first. Ensure that your rent/mortgage, utilities, food, and critical business expenses are covered before allocating funds to discretionary spending or long-term goals. This ensures your basic needs and business operations are always secure, even when income dips.

Staying on Track: Regular Review and Adjustment

A budget is not a static document; it is a living, breathing financial tool that requires regular attention and adaptation. The financial landscape of self-employment is constantly changing, with new projects, unexpected expenses, and shifting market conditions impacting your cash flow. Therefore, consistent review and adjustment are paramount to its effectiveness.

Schedule dedicated time each month to review your budget. Compare your actual income and expenses against your planned figures. Identify any discrepancies, large or small, and understand the reasons behind them. Did you earn more than expected? Did an unforeseen business expense crop up? This monthly check-in is crucial for accountability and learning.

Beyond monthly reviews, conduct a more comprehensive assessment quarterly or annually. This longer-term perspective allows you to re-evaluate your financial goals, adjust your savings targets, and reassess your business expenses in light of your evolving business strategy. It’s an opportunity to fine-tune your financial plan for the year ahead.

Flexibility is a key attribute of a successful self-employed budget. Life happens, and your business evolves. Don’t be discouraged by occasional setbacks or months where you don’t perfectly adhere to your plan. The purpose of a budget is to provide guidance, not to impose rigid restrictions that lead to frustration. Learn from deviations and adapt your approach.

Remember that continuous improvement is the goal. Each review cycle provides valuable insights that help you refine your financial habits and make better decisions moving forward. Embrace the iterative process, and you’ll find that your budget becomes an increasingly powerful tool for achieving financial freedom and success in your self-employed journey.

Frequently Asked Questions

How often should I update my self-employed budget?

You should review your budget at least once a month, comparing your actual income and expenses against your planned figures. This allows you to catch discrepancies early and make necessary adjustments. A more comprehensive review, perhaps quarterly or annually, is also beneficial for long-term goal setting and financial strategy alignment.

What if my income is extremely unpredictable?

For highly unpredictable income, consider using strategies like the “buffer account” method (saving extra in high-income months to cover lean ones) or budgeting based on your average income over the last 6-12 months. You can also create tiered budgets with different spending limits for high, medium, and low-income months to maintain flexibility.

How much should I set aside for taxes?

The exact amount varies based on your income, deductions, and state tax laws. A general rule of thumb for federal self-employment tax is to set aside around 25-35% of your gross income, but consulting a tax professional for personalized advice is highly recommended. This percentage should cover both income and self-employment taxes.

Should I combine personal and business budgets?

While an integrated template helps you see your overall financial picture, it’s crucial to maintain separate bank accounts for personal and business finances. Within your budget, clearly delineate between personal and business income and expenses. This separation is vital for accurate accounting, tax preparation, and understanding your business profitability.

What’s the best tool for this kind of financial tracking?

The “best” tool depends on your preferences. Many self-employed individuals use spreadsheets (like Excel or Google Sheets) for their flexibility and customization. Alternatively, dedicated budgeting apps and small business accounting software (like QuickBooks, FreshBooks, or YNAB) offer automation features, bank integration, and robust reporting for more comprehensive management.

Adopting a robust financial management system is arguably one of the most impactful decisions you can make as a self-employed individual. It transcends simple accounting, becoming a profound act of self-care and strategic foresight. By bringing order and clarity to your money, you unlock the mental space and resources needed to focus on what you do best: growing your business and pursuing your passions.

Don’t let the complexities of self-employment finances deter you from achieving your full potential. Embrace the power of a well-structured budget to transform your financial life, providing the stability and confidence required to thrive. Start today by organizing your financial data and committing to a consistent review process; your future self, and your business, will undoubtedly thank you for it.